Installment payments in Latin America for foreign companies

Discover how Rebill enables you to charge your customers in installments in Latin America, improving your acceptance rate and optimizing your transactions with local payment methods.

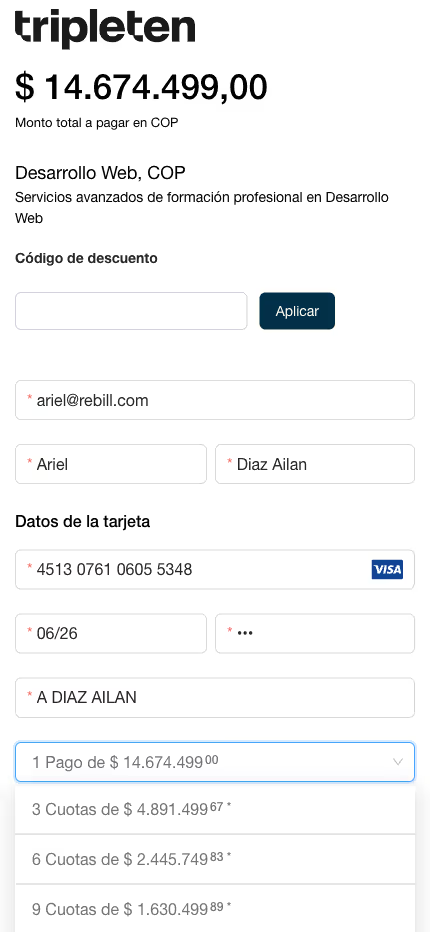

Increase your sales with installment payments

In Latin America, installment payments are an essential tool to increase average purchase value and attract more customers. Rebill offers flexible solutions to manage installment payments, allowing companies to adapt to local preferences and improve their cash flow.

Benefits of using Rebill to accept installment payments

Installment payments with local cards

Allow your customers to finance their purchases in installments using local Latin American cards, increasing the average purchase value and benefiting your business. Rebill supports installment payments in key countries such as Brazil, Mexico, Colombia, Argentina, and Chile.

Flexible settlement according to your operating model

Rebill allows businesses to choose between receiving the total sale in a single payment while customers pay in installments, or receiving installment payments together with customers. Both modes are available to suit your business needs.

International installment charges

Companies in multiple countries, such as the United States, can charge Latin American customers in installments in their local currencies and receive USD in their home country, without the need for a local entity in each country where they have customers.

Latin America installment payment market data

.avif)

Brazil

It is the largest e-commerce market in Latin America, with a high use of installment payments. Around 60% of online purchases are made through installment plans.

Mexico

In Mexico, installment payments are a popular option in e-commerce. Approximately 65% of consumers prefer to pay in installments.

Colombia

In Colombia, installment payments represent approximately 30% of online purchases.

Argentina

Argentina has a long tradition of installment payments, being one of the preferred methods by consumers. Around 60% of online transactions are made through credit cards with multiple installments.

Chile

In Chile, credit card installment payments are widely used. The schemes operate through the main local networks, with typical terms of 3 to 12 months and settlement in Chilean pesos.

Why offer installment payments in Latin America

Increase in average ticket

The use of installment payments allows consumers to make higher-value purchases, which increases the average ticket for businesses. By offering financing options, companies can attract more customers and increase revenues.

Solutions adapted to various industries

Rebill adapts to the needs of diverse industries, including tourism, technology, education, and more, allowing companies to offer financing plans that fit their business models.

Simple and efficient implementation

Integrating installment payment solutions with Rebill is easy and efficient. Our platform offers integration with multiple payment methods and ongoing support to ensure your collection system runs smoothly.

How installment payments work in Latin America

Installment plans in Brazil

Installment payments are the native payment method in Brazil. The card issuer finances the transaction and divides it into monthly installments; the merchant receives the consolidated payment within a typical period of 30 to 33 days. Installment payments account for more than 60% of credit card volume in the country and are a de facto requirement for selling medium- to high-ticket items.

MSI (Interest-Free Months) in Mexico

In Mexico, the standard scheme is Meses Sin Intereses (MSI, or Interest-Free Months). Unlike the Brazilian installment plan, the financial cost is absorbed by the merchant through an additional discount rate agreed upon with the acquirer. The availability of MSI varies depending on the issuing bank: not all issuers enable MSI for all merchants or for all terms (3, 6, 9, 12, or 18 months).

Quotas in Argentina

In Argentina, credit card installments operate under a scheme where the financial cost may be subsidized by the issuer in promotional plans, or absorbed by the merchant in permanent plans. Exchange rate dynamics and currency controls mean that settlement is in Argentine pesos, with direct implications for companies that need to settle in USD.

Operating with a local entity: how quotas work

Having a registered entity in the target market provides direct access to local acquirers and the native payment terms in each country. It involves hiring a local acquirer or gateway, complying with the country's tax and corporate requirements, and managing settlements in local currency.

Settlement times by market

In Brazil, the typical settlement for the first installment is D+30 to D+33, with subsequent installments on a monthly basis. In Mexico, the total amount is settled on D+1 to D+3 (the issuing bank finances the installments to the merchant). In Argentina, the terms range from D+2 to D+5 depending on the acquirer, with additional variability due to exchange controls.

Operational considerations for local authorities

Operating with a local entity requires: bank accounts in local currency, active tax compliance (CNPJ in Brazil, RFC in Mexico, CUIT in Argentina), FX management only on repatriation, and a reconciliation system capable of cross-referencing multiple installment events against a single sales event. The operating break-even point is usually between USD 300k and USD 800k in monthly volume.

Operating without a local entity: offering cross-border quotas

Without a registered entity in the target market, the alternative is to operate via a PSP that acts as an intermediary with local acquirers under its own license. The merchant does not need a local company or bank account in the country: the PSP manages the acquirer, local settlement, FX conversion, and hard currency remittance.

Settlement and conversion in the cross-border model

The PSP converts the funds into local currency and remits them in USD or EUR. FX spreads vary between 1% and 3.5% depending on the market and the volume traded. The IOF tax in Brazil for international card transactions can be around 3.5%, which impacts the total cost of processing cross-border payments. In Argentina, there are regulatory restrictions on foreign currency outflows, which the PSP or MoR manages on behalf of the merchant.

Advantages and limitations of the cross-border model

The main advantage of the cross-border model is the speed of market entry. A foreign company can start processing payments in Latin America without setting up a local entity or signing direct contracts with acquirers in the country.

The main limitation is that the business depends on the PSP's infrastructure for access to local acquirers. This can mean higher processing costs and less control over transaction routing or direct relationships with issuers in the market.

Comparison of models: local entity vs. cross-border

The choice between local and cross-border entities depends on the volume processed, the target markets, and tolerance for regulatory complexity. The key factors to evaluate are as follows.

Complexity of implementation and time to market

With a local entity, the setup includes company incorporation, opening accounts, tax registration, and a contract with the acquirer: between 3 and 9 months depending on the country. With cross-border, integration with an authorized PSP can be completed in 1 to 4 weeks.

Processing and FX costs

The local model has lower acquisition costs, but adds a fixed compliance and accounting structure. The cross-border model consolidates everything into the processing cost, eliminating the fixed structure but with additional FX spreads.

Approval and reconciliation rates

Local acquirers often have direct relationships with issuers in the market, which in many cases translates into better approval rates compared to international processing. This is due to factors such as knowledge of market behavior, integration with local networks, and optimization of routing to domestic issuers.

In terms of reconciliation, operating with local acquiring may involve managing settlements from different acquirers and settlement cycles depending on the market and payment method. In cross-border models, the PSP often acts as an intermediary and consolidates payment and settlement information into unified reports, simplifying operational reconciliation for merchants.

Model with local entity:

• Local procurement

• Settlement in local currency

• Less friction in local emitters

Cross-border model:

• No local entity required

• International payment infrastructure

• Consolidated settlement in USD

What payment infrastructure is needed to offer installments in Latin America?

Enabling reliable installment payments in Brazil, Mexico, and Argentina requires more than just accepting Visa and Mastercard. The relevant infrastructure covers three areas: access to local networks, routing logic, and installment reconciliation.

Access to local payment networks

In Brazil, the relevant networks are Elo, Hipercard, Hiper, and local Amex. In Mexico, Carnet and issuers authorized in PROSA for MSI. In Argentina, Cabal, Naranja, and networks operated by major local banks. Without connection to these networks, access to installments is limited to international Visa and Mastercard BINs, which have less coverage of installments with local issuers.

Smart routing for quotas

Routing determines which acquirer processes each transaction. Incorrect configuration can result in the processing of a card enabled for installments without activating the installment plan, or in avoidable declines due to lack of fallback. Optimal logic evaluates the issuer's BIN, the number of installments requested, the transaction amount, and applies automatic fallback rules per acquirer.

Reconciliation of installment payments

The reconciliation of installment payments varies depending on the scheme used by each market and issuer. In some models, the merchant receives the total amount in a single settlement while the customer pays in installments to the issuing bank. In others, payments are settled in monthly cycles corresponding to each installment.

To operate at scale in Latin America, the reconciliation system must be able to link each transaction to its installment plan, the acquirer used, the market of origin, and the settlement currency. This allows for consistent reporting by country and currency, and maintains accounting traceability even when payments are processed in local currencies but consolidated in USD.

Frequently asked questions about installment payments in Latin America

Can foreign companies offer installment payments in Latin America?

Yes, but the operating model determines the scope. With a cross-border PSP or Merchant of Record, a foreign company can offer fees without having a local legal entity. With local acquiring, incorporation in the country and direct contracts with acquirers are required.

Which countries use installment payments the most?

Brazil leads the way with installment plans, which account for more than 60% of credit card volume. Mexico operates with interest-free months (MSI) through the main issuing banks. Argentina has a long tradition of card installments, conditioned by exchange rate dynamics. Chile shows sustained growth in the adoption of installments in e-commerce.

Who absorbs the financial cost of the fees?

It depends on the model. In the standard model, the merchant assumes the cost of financing through a differentiated MDR. In models such as MSI in Mexico, the cost is distributed between the merchant and the issuing bank according to the agreed scheme. Rebill allows this distribution to be configured according to the conditions of each market.

Can it be settled in USD if the customer pays in local currency?

Yes. Rebill manages currency conversion. The customer pays in their local currency (MXN, ARS, CLP, BRL), and the merchant receives settlement in USD. The conversion spread (FX) is applied at the time of the transaction.

Is a local entity necessary to offer installment payments in Latin America?

No. Rebill operates under a cross-border model, which allows it to process installment payments without establishing a legal entity in each country. The installment scheme requires access to local processing networks, which Rebill already has in place in the region's main markets.

Ready to collect in installments?

Rebill is positioned as the ideal partner for managing installment payments in Latin America, offering a robust and secure platform that supports a wide variety of local and alternative payment methods, allowing companies to maximize their reach and improve their cash flow.

.avif)