Blog

Automating Recurring Payments in Latin America: A Guide to Reducing Manual Work and Recovering Failed Payments

A Comprehensive Guide to Automating Recurring Payments in Latin America. Dunning, recovery of failed payments, local payment methods, and best practices for digital businesses.

All publications

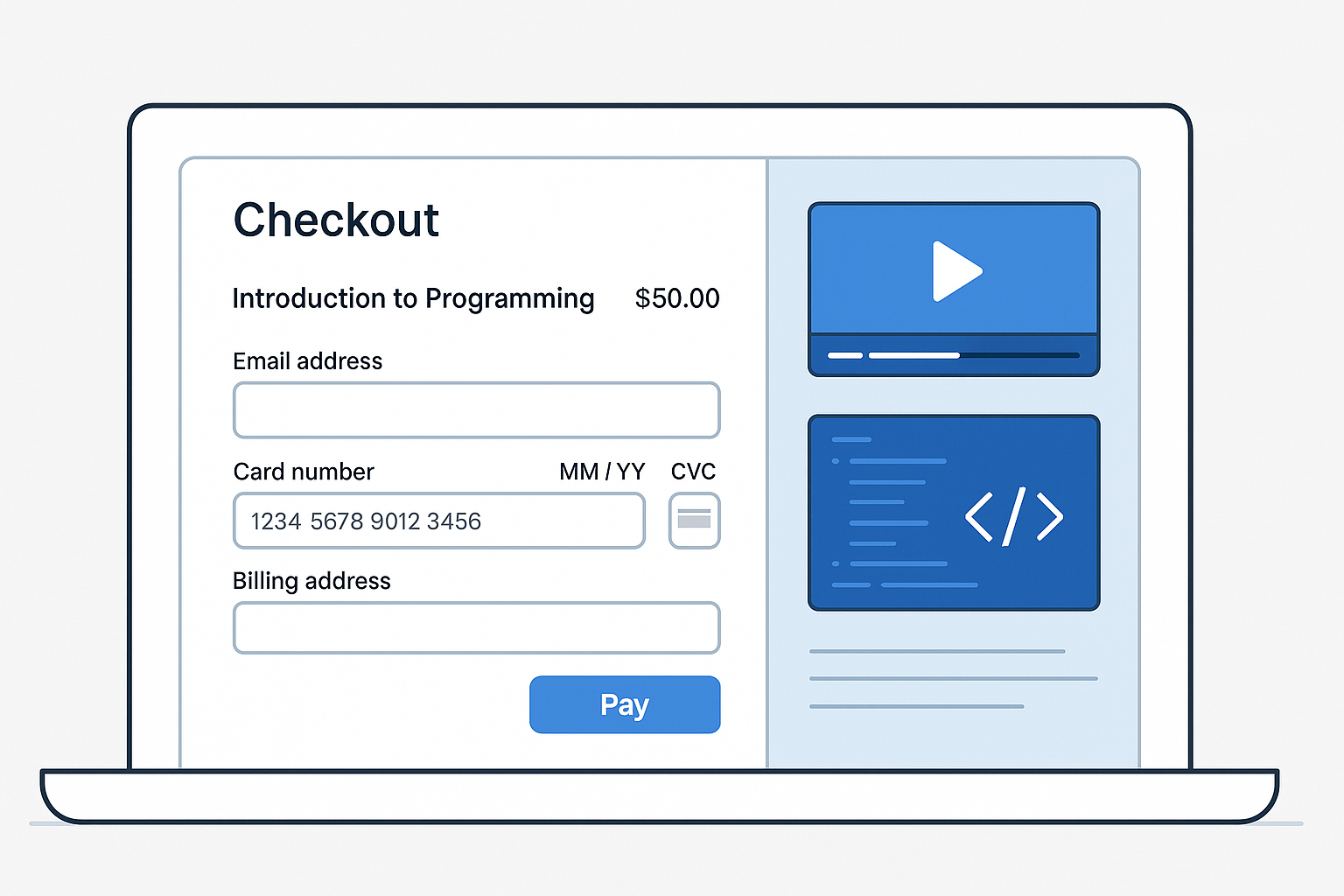

During the purchase process in an online store , the customer must complete a very important step called checkout. Knowing what it is and how it works will help optimize this stage to generate a good shopping experience and a successful sale.

What is checkout?

This is the last step of the purchase process in which the customer confirms the products he/she wishes to pay the store or e-commerce business for.

At this stage, the customer selects the payment method, confirms the shipping address and finalizes the online purchase. However, a poorly designed checkout page can lead to cart abandonment, affect the results and decrease the conversion rate of an online store.

What are the types of checkout that exist?

There are different types of checkout available for a customer to finalize their purchase:

- Traditionalcheckout: the customer has a form with step-by-step instructions on what to do, such as reviewing the cart, personal information, choosing the shipping option, payment method, confirming data and processing payment.

- Single-pagecheckout: all the information needed to complete the purchase is on the same web page, without redirection, offering a simpler and faster experience.

- Multi-stepcheckout: the customer must go through several stages during the purchase, which implies a longer process, more clicks and a higher probability of abandonment.

- Socialcheckout : the retailer uses social networks as a sales channel and completes the purchase process without leaving the applications.

- Checkout APICheckout API: the buyer does not have to leave the site, since the online store has the payment provider integrated into its page. Once the customer decides to buy, the API manages the data collection.

How does the checkout process work?

A good e-commerce checkout must follow these steps to complete a purchase:

- Product selection in the shopping cart: the customer checks his cart before proceeding to checkout.

- Choice of shipping method: choose from the available options the most convenient one, depending on shipping costs and delivery times.

- Registration of personal data and shipping address: enter in the payment page your data for the transaction and the place of reception of the product.

- Selection of the payment method: choose from the multiple options available such as credit or debit card, transfer or virtual wallet.

- Confirmation of the purchase and payment experience: notifies the customer that the purchase process was successfully completed and requests the customer's evaluation of the experience to correct any errors that may have occurred in the future.

Why is security important in the checkout process?

A secure payment gateway with SSL (Secure Sockets Layer) protects the customer's personal and financial data by ensuring that it cannot be read by intruders or hackers, and that the information will not be modified during a transaction.

The security it provides to the customer reinforces trust in the online store, improves the shopping experience by offering a smooth and seamless checkout process. It also increases the conversion rate and reduces the purchase abandonment rate.

8 best practices for checkout optimization and customization

Improving the checkout of an online store is possible with these best practices:

- Reduce form fields and use autocomplete: requesting only the basic information to make the purchase and having the function to automatically complete the text helps save time and avoids errors.

- Offer payment options and multiple means of payment: have available as many options as possible, such as credit cards, debit cards, prepaid cards, transfers, installment payments, mobile device payments, wallets, so that the customer can choose the one that best suits him/her.

- Show clear information on how the shipments are: clarify what the waiting times are, if there is an additional charge and the shipping method, especially if they are international.

- Ensure transparency of personal data and use of SSL protocols: allows the information to be encrypted and guarantees its integrity during the transaction.

- Personalize the user experience to improve the shopping experience: each customer has their own needs, the strategy must be adapted according to their preferences and behavior in the online store.

- Use strategies to reduce shopping cart abandonment and recover abandoned carts: simplify the checkout process, automate reminder emails, and offer various payment methods. Rebill’s smart retries and automatic notifications help recover about 52% of declined payments.

- Constantly test to reduce the abandonment rate and improve the conversion rate: test the page or the checkout process to verify its performance and identify errors that may interfere with the purchase.

- Provide support in real time and guarantee attention at key times: provide immediate assistance to solve doubts or guide the customer in the final phase so that he/she has a good buying experience.

Rebill is the best payment platform for global companies, with presence in several Latin American countries. Thanks to it, customers will have a payment environment to process purchases in a secure and personalized way, with local and international options.

Why use Rebill checkout in your business?

With Rebill checkout you will make a difference in your business and improve the customer experience thanks to these advantages:

- Hyper-customizable checkout: customize the design with your logo, colors and domain, offering an experience aligned with your brand and increasing customer trust.

- Mobile optimization and seamless experience: Rebill's one-click payments are designed for mobile and reduce friction, speeding conversion and reducing cart abandonment.

- Automatic notifications and cart recovery: reminders via WhatsApp or email help customers finalize pending payments, increasing the success rate of your transactions.

- Fast and easy integration: with modern SDKs and REST APIs, you can deploy Rebill in your business in less than an hour, without relying on complex development.

- Intelligent and multi-currency payment links: each link automatically adapts to the client's currency and country, allowing you to charge in Argentina and other LATAM markets without complications.

- Recurring and flexible billing: set up subscriptions, upgrades, downgrades and trial periods from the same payment link, ideal for recurring services or online courses.

If you want to have a secure checkout process, keep your customers on your site and reduce chargebacks in your business, contact us, we have a hyper-customizable checkout for you!

dLocal vs. EBANX vs. Rebill: Which Platform Works Best for Accepting Payments in Latin America

Quick Answer: For foreign companies looking to accept payments in Latin America, dLocal and EBANX excel at multi-country enterprise operations, while Rebill is a better fit for digital companies (SaaS, EdTech) that need local payment methods, subscriptions, and billing with quick integration—and it allows you to accept local payments without establishing legal entities in each country. The best option depends on your target countries, whether your billing is recurring, and how quickly you need to get up and running.

Many companies trying to sell in Latin America run into the same problem: the product works, the market exists, but payments aren't going through.

Part of the challenge is technical (methods and approval), and part is operational (how easy it is to manage returns, reconciliation, and reporting). In this context, there is one factor that often unlocks expansion for foreign companies: Rebill allows them to accept local payments in Latin America without having to establish legal entities in each country.

- Domestic cards and international payments: Many customers use locally issued cards that don't always work well in international transactions (due to issuer rules, anti-fraud measures, or spending limits).

- Local payment methods: In many countries, in addition to credit cards, shoppers expect bank transfers, digital wallets, and local payment options. If you don't offer them, you'll miss out on potential customers.

- Installment plans: In some markets, installment plans are a common purchasing practice. For certain purchase amounts, not offering installment plans reduces sales volume.

- Lower approval rate for cross-border transactions: even with a good product, charges processed as “international payments” tend to have a lower approval rate than equivalent domestic charges.

That’s why choosing the right provider can have a direct impact on conversion rates and regional expansion. For a general overview of the mix of payment methods by country, check out our guide to payment methods in Latin America and our guide to payment gateways in Latin America.

If you're comparing dLocal and EBANX, you're likely evaluating how to accept payments in Latin America as an international company. Alternatives like Rebill often come up during this process, especially when the goal is to launch faster with local payment methods and a streamlined operational integration.

Why Payments Work Differently in Latin America

Latin America is not a single market. If your goal is to sell in multiple countries, these differences become crucial:

Actual fragmentation by country. Each country has its own mix of banks, payment processors, alternative payment methods, and payment habits. A checkout optimized for Mexico may not work the same way in Brazil or Colombia.

Preference for local payment methods. In some cases, it’s not a matter of “preference” but of accessibility: some customers cannot (or do not want to) pay with an international card and end up using bank transfers or digital wallets.

Installment plans as part of the purchasing process. In certain segments, buyers make their decision based on whether they can pay in installments. This affects price elasticity and the purchase rate.

Regulatory and operational differences. Onboarding, controls, and the process for settling funds can vary by country and business model. This affects both timing and complexity.

Direct impact on conversion rates. When the payment method isn't what customers expect, rejection rates and cart abandonment rates rise. In terms of growth, it's a silent drain.

Quick Comparison: Rebill vs. dLocal vs. EBANX

If you're comparing dLocal and EBANX, this table summarizes the key differences at a high level. This is not a ranking: the best option depends on your business model, target countries, and payment method.

| Feature | Rebill | dLocal | EBANX |

|---|---|---|---|

| Product Overview | Payment platform focused on Latin America for digital companies | Global platform for emerging markets | Payment platform focused on international trade with Latin America |

| Local payment methods | Yes | Yes | Yes |

| Recurring payments / subscriptions | Yes, with full support | Limited / depends on the case | It is not their main focus |

| Installment Payments | Yes | It depends on the country | It depends on the country |

| Integration speed | Quick | Enterprise onboarding | Enterprise onboarding |

| Typical customer profile | SaaS, EdTech, digital services | Major global companies | International trade with Latin America |

| Need for a local entity | Not necessarily | It depends on the model | It depends on the model |

The comparison above outlines general differences. In practice, the choice depends on your business model, your target countries, and whether you need recurring payments or specific local payment methods.

First-party data and transparent pricing

One specific advantage of Rebill is its price transparency: it publishes its rates by country and payment method, whereas dLocal and EBANX do not publish their prices (custom/enterprise plans). Rebill’s published rates by payment scenario: cross-border, Argentina, Mexico, Chile, Colombia, and the United States.

Some data on Rebill’s operations (June 2026): automatic retries recover about 52% of subscription charges that fail due to insufficient funds; the mix of payment methods varies significantly by country (in Brazil, Pix accounts for ~82% of approved charges; in Colombia, PSE accounts for ~48%); and where installment plans are offered, the average transaction amount for installment payments can be up to ~4x that of a single payment.

Pros and cons of each platform

This section summarizes the typical advantages of each option. It is not a substitute for a technical evaluation, but it can help you make a decision if you are comparing dLocal and EBANX and want to include Rebill in your analysis.

Pros of Rebill

- Focus on digital companies (SaaS, EdTech, and online services) that need to collect payments quickly across multiple countries.

- Rebill allows you to accept local payments in Latin America without having to set up legal entities in each country.

- A good fit when your business involves recurring transactions and you need clear operations: reconciliation, refunds, and reporting.

- Support for local methods and quotas where they are relevant for conversion.

Pros of dLocal

- A provider with a global presence and experience in multi-country enterprise projects.

- Extensive coverage in emerging markets, which is useful if you're expanding regionally and beyond Latin America.

- This is a common scenario when the company already has internal compliance and enterprise procurement processes in place.

Pros of EBANX

- A strong historical focus on Latin America, with a particular emphasis on Brazil.

- A popular choice for international businesses that sell to the region and need local payment methods.

- This is useful if Brazil is a priority market and you want to improve conversion rates using local methods.

What is Rebill?

Rebill is a payment platform designed for businesses looking to sell in Latin America, offering a user-friendly setup and a strong focus on operational efficiency: reconciliation, return management, and clear reporting.

In terms of capabilities, it typically focuses on:

- Acceptance of local payment methods by country.

- Subscriptions and recurring payments for businesses with monthly or annual billing (such as SaaS or EdTech).

- Installment payments where they are a conversion factor.

- Rapid integration for product and engineering teams that need to get to production without lengthy cycles.

- Support for key markets such as Argentina, Mexico, Brazil, and Colombia.

Key differentiator: Rebill enables companies to accept local payments in Latin America without having to establish legal entities in each country (depending on the country and the payment structure). For many foreign companies, this is the factor that unlocks expansion when their business plan needs to move faster than the process of setting up legal entities.

What is dLocal?

dLocal is a global payment-focused provider serving emerging markets. It is frequently considered in enterprise evaluations due to its regional coverage and its experience working with international companies that need to operate in multiple countries.

In practice, dLocal tends to work well when:

- The operation spans multiple countries and involves strict corporate requirements.

- The team is prepared for a more enterprise-level onboarding process (timelines, compliance, volume-based agreements, and country-specific requirements).

- The company is looking for a solution with a global presence to expand beyond Latin America.

What is EBANX?

EBANX is a provider focused on Latin America, with a long-standing strong presence in Brazil and a service offering centered on international commerce that it aims to expand throughout the region. For many companies, it emerges as a direct alternative in comparisons between dLocal and EBANX, especially when Brazil is a priority market.

In practical terms, EBANX is typically considered when:

- Brazil plays a major role in the expansion plan.

- The company is looking to incorporate local strategies in Latin America to improve conversion rates.

- This is a cross-border sale, so you need to work with a supplier experienced in international transactions.

Comparison by key criteria

To avoid superficial comparisons, it is best to evaluate based on criteria that actually impact operations and conversion rates.

Local payment methods

Local payment methods are critical because they expand coverage and can improve approval rates. In practice, the goal is for the customer to find a familiar option and for the payment to be clearly confirmed.

What to check:

- Whether the provider covers the actual mix by country (not just “cards”).

- What is the user flow like (e.g., confirmation, expiration, and retries)?

- How easy it is to reconcile later: an order can be tracked from checkout to the warehouse.

Country-specific guides that can help you get a handle on the situation: payment gateways in Brazil and payment gateways in Colombia.

Subscriptions and Recurring Payments

In SaaS and EdTech, it’s not enough to simply collect the first payment. What matters is maintaining a steady stream of monthly payments through effective error handling: retries, card updates, expiration management, and traceability for support.

When comparing them, there are usually differences:

- Platforms focused primarily on recurring revenue (with comprehensive tools).

- There are platforms where recurring payments are available, but this depends on the country or the specific situation.

Installment Payments

Price points are important when the product calls for them or when they are standard in the market. If your product competes on price and accessibility, price points can be a deciding factor.

What to evaluate:

- Actual availability by country and payment method.

- A seamless user experience (selecting rates, costs, and confirmation).

- Reflected in reports: so that the finance department can understand the final amount and the fees.

Related reading: Fees for foreign companies in Argentina.

Integration and implementation

What matters here is the actual cost of getting into production and operating smoothly. It’s not just about “having APIs.” It’s about timelines, documentation, and what happens after payment.

Practical checklist:

- Typical implementation and go-live timeline.

- Technical documentation and support.

- Automatic payment notifications (webhooks) and retry handling.

- Downloadable reports and identifier consistency.

Here's a simple example: a transaction should show how much was charged, what fee was deducted, and how much was deposited. If you can't easily piece that information together, the process becomes manual.

Geographical focus

The ideal platform depends on your actual plan:

- Are you going to start with 1 or 2 countries, or do you need broad coverage right from the start?

- Do you have a “primary” country (such as Brazil) where you need the best performance?

- Is your model recurring, one-time, or a combination of both?

Which platform to choose based on your type of business

SaaS

For SaaS, the key considerations are typically: subscriptions, consistent billing, clear support processes, and integration that doesn’t hinder go-to-market efforts. If your expansion is gradual, a quick implementation using local methods is usually a priority.

EdTech

EdTech shares many of the same requirements as SaaS, but with two key differences: tickets that can be purchased in bulk and a hybrid sales process (self-service and assisted sales). In this context, the mix of methods and the payment experience are particularly important.

Marketplaces

On marketplaces, the challenge lies in ensuring traceability: returns, adjustments, reconciliation, and clear rules. When you factor in multiple countries, the complexity increases rapidly, so it’s important to prioritize operational control.

International e-commerce

In international e-commerce, the focus is typically on conversion. It’s important to prioritize local payment methods, clear confirmations, and reports that provide insight into the total cost per method (including fees, returns, and chargebacks, if applicable).

How to choose a payment gateway for Latin America

Before making a decision, break it down into a checklist that any team can follow:

- Target countries: Define the actual order of expansion and your main country.

- Required methods: Validate the payment mix by country (credit cards, bank transfers, digital wallets, installments).

- Business model: If it is a recurring model, evaluate specific subscription capabilities.

- Implementation time: whether it takes weeks or months makes all the difference.

- Support and Operations: Ask for examples of reports, return processing, and real-world scenarios.

To learn more about the regional context, you can also check out digital wallets in Latin America.

Frequently asked questions

What is the best payment gateway for Latin America?

There isn't a single "best" option. The best one is the one that fits your target countries, the methods you actually need, and your business model (recurring or one-time payment). In practice, it's best to prioritize conversion rates and ease of use.

How can a foreign company accept payments in Latin America?

There are two common approaches: accepting international payments (simpler, but typically with lower approval rates) or accepting local payments using local payment methods (better coverage, but requires a suitable provider). See guide: Payment Methods in Latin America.

What payment methods do customers in Latin America use?

It depends on the country and the segment, but in addition to credit cards, local bank transfers, digital wallets, and, in some markets, installments are also common. See: Payment Methods in Latin America.

Is it necessary to set up a local company to accept payments in Latin America?

Not always. It depends on the country, the payment method, and the provider’s structure. If your plan requires speed, it’s worth exploring options that allow you to process payments locally without setting up entities in each country.

What should I ask for in a technical evaluation?

Rather than just a demo, ask for documentation, examples of actual reports, and the complete transaction flow (from order to deposit). If that part isn't clear, problems will arise later during operations.

Alternatives to dLocal and EBANX

In addition to dLocal and EBANX, there are other payment platforms focused on Latin America. Some are designed for large companies with complex operations and a presence in many markets, while others prioritize speed of implementation and support for digital businesses.

In practice, many foreign companies that compare dLocal and EBANX end up also evaluating specialized Latin American alternatives that allow them to launch local payment methods with less operational friction.

Platforms such as Rebill and other alternatives to dLocal and EBANX focus on helping SaaS companies, EdTech firms, marketplaces, and digital service providers accept local payments in Latin America without having to establish legal entities in each country.

This approach can be particularly useful when the goal is to launch quickly in markets such as Mexico, Brazil, Colombia, or Argentina and validate conversion rates before establishing a more complex local infrastructure.

Conclusion

Rebill allows you to accept local payments in Latin America without having to set up legal entities in each country. If your expansion plan depends on moving quickly, this factor is key when comparing options.

The question of whether to choose dLocal or EBANX typically arises when a company has decided to seriously expand into Latin America. The right decision isn’t about “which one covers more countries,” but rather which one best fits your specific needs: target countries, key features, subscription plans (if applicable), pricing, and the time you have to implement the solution.

In practice, it’s best to use a simple criterion: Can you improve conversion rates without creating an operational problem down the line? A good platform doesn’t just help you collect payments; it also helps you understand what happened with each payment, what was deducted, and what was deposited.

Payment Gateways in Brazil (2026): A Comparison for Businesses

Quick answer: In Brazil, the best payment gateway combines Pix, credit cards (with installments), and Boleto, with local acquiring to boost approval rates and clear settlement for reconciliation. Pix already accounts for the majority of online volume, so prioritizing it—without neglecting reconciliation by identifier—is what has the greatest impact on conversion and total cost.

Choosing a payment gateway in Brazil is about more than just “accepting cards.” In practice, it determines which payment methods you offer, how user-friendly the checkout process is , how funds are settled, and how automated the accounting reconciliation can be.

In this technical guide, we review how online payments are structured in Brazil, the most commonly used methods, and what to look for when selecting a provider. For a regional overview, see payment gateways in Latin America. If your business involves international payments, see international payments.

In Brazil, it is often necessary to design the checkout process by payment method: Pix, credit cards, and payment slips each have different processing times, fees, and reconciliation procedures.

The goal for companies is to maximize conversion without compromising control over settlement, adjustments, and returns.

If you're an international user, make sure the service is compatible with local payment methods and that exchange rates (FX) are clearly stated before making your choice.

How online payments work in Brazil

In a typical e-commerce workflow, your website or app captures the payment intent, sends the transaction to the provider, and the provider handles the authorization (credit card or bank transfer), confirmation, and subsequent settlement. The difference between providers lies not only in “whether they approve” the transaction, but also in how they present events, references, and reports for operating in Brazil.

For businesses, the most critical issues are typically: issuer approval, fraud and chargeback management, settlement times, availability of reports, and consistency of identifiers for reconciliation.

Most Common Payment Methods in Brazil

In Pix, traceability depends on identifiers and references: make sure you can link order → payment → statement.

In the ticket, configure expiration, cancellation, and inventory settings. Deferred payments change the customer experience.

The mix of methods varies by industry, average order value, and sales channel. In general, it’s usually best to prioritize the methods that maximize conversion without compromising operational control: traceability, reconciliation, and returns management.

- Pix: An instant and dominant method: it accounts for about 82% of transactions in our Brazilian operations. It improves cost efficiency and reduces chargebacks, but requires reconciliation by identifier.

- Credit Cards: The foundation of e-commerce, with a high proportion of installment payments (nearly 69% of credit card payments in Brazil are made in installments) and authorization by the issuer.

- Ticket: Useful for certain segments and tickets: affects confirmation times and cancellations.

- Wallets: They complement mobile conversions; it’s usually a good idea to measure their impact by channel.

A best practice is to set up tracking for the checkout process to measure conversion rates by payment method, rejection rates by issuer, and confirmation times. This allows you to choose a provider based on data, not just on the published rate.

The leading payment gateways in Brazil

Since there isn't a single winner, prioritize operational fit: data, automated notifications (webhooks), reports, and support. That's what defines scalability.

This list is for informational purposes only and is not a ranking. The exact availability of payment methods, terms and conditions, and technical support varies depending on the specific case and volume.

- PagSeguro: A Brazilian provider of online payment processing services with local options.

- Mercado Pago: Checkout for merchants using credit cards and local payment methods, depending on the configuration.

- Pagar.me: A payment platform and gateway focused on integrations for businesses in Brazil.

- Stone: Payment solutions for merchants with e-commerce and POS capabilities.

- Cielo: A provider of solutions for retail and e-commerce.

- EBANX: Specialist in local payment methods in Latin America (including Brazil) for global merchants.

- Rebill: A platform for accepting payments in Brazil using local payment methods, with a focus on reconciliation, fund settlement, and recovery of rejected payments (see details below).

- Stripe: APIs for credit card processing; availability by country and use case.

- Adyen: A platform for large companies that supports multiple payment methods and local payment methods.

- dLocal: Access to local payment methods for international transactions or platforms.

- Getnet: Payment acceptance solutions for merchants.

Before making a decision, request API documentation, payment event notifications (webhooks), sample settlement reports, and a clear breakdown of the fees charged (fees, fixed per-transaction charges, chargebacks, anti-fraud fees, refunds, and foreign exchange (FX) rates, if applicable).

Rebill in Brazil: Advantages and Limitations

Rebill is a payment platform for businesses that accept online payments at scale. It operates in Argentina, Brazil, Chile, Colombia, Mexico, and the United States: it allows Brazilian companies to accept payments in reais and international companies to accept payments in BRL and settle in USD overseas, depending on the structure of the transaction.

Advantages

- Local payment methods in Brazil in a single checkout: Pix, credit card (with installments), and Boleto, with reconciliation on a per-transaction basis.

- Recovery of Declined Payments: Through retries and a recovery window, it recovers approximately 52% of transactions that initially fail and improves the approval rate by up to 20% above the average.

- Reconciliation and settlement with consistent identifiers, reliable webhooks, and reports that break down net amounts, commissions, and settlements.

- Customizable checkout, payment links, and subscription management with no extra fees for these features.

- Designed for the real Brazilian market: Pix dominates (accounting for about 82% of transactions) and installment payments are significant (accounting for about 69% of card payments), and both are natively supported.

Limitations

- It is not an in-person payment solution: it does not offer a physical POS terminal; it is designed for online and recurring payments.

- It is not a payment processor in and of itself: it orchestrates local payment methods and gateways, so the exact availability of each method depends on the configuration and the specific situation.

- If you just need a simple, low-volume payment button, this is more platform than you'll likely need.

How to Choose a Payment Gateway in Brazil

For businesses, the selection process should be based on operational and risk requirements. A practical checklist:

- Required methods: Cover the actual payment mix (card, Pix, payment slip, digital wallet) without increasing the number of reconciliations.

- Conversion: Delay, Friction, Retry, and Authentication Policies.

- Settlement: schedule, currency, fee discount prior to settlement (netting), and availability of transaction-level details.

- Reconciliation: Consistent, exportable IDs; reliable webhooks; and reports that break down net amounts, commissions, and settlements.

- Risk: additional verification support (3DS), anti-fraud tools, chargeback management, and rules by issuing bank (BIN)/country.

- Scalability: limits, API stability, agreed-upon response times (SLA), and support for high demand.

In Brazil, Pix and fees mean that the “total cost” is more than just the credit card interest rate.

Payment gateway fees in Brazil

There is no such thing as a “single commission.” The total cost typically consists of: a variable rate (percentage), a fixed fee per transaction, costs related to chargebacks, refunds, and fraud prevention, and—for international transactions—the exchange rate (FX) and bank fees.

To compare providers, request a breakdown of the net amount settled per transaction (settlement example) and simulate different payment method mix scenarios. A payment gateway with a slightly higher rate may be more efficient if it improves approval rates and reduces chargebacks.

Operations and Reconciliation: What Data You Need in Brazil

Beyond the checkout process, issues often arise in the back office: reconciliation, refunds, adjustments, and reporting. A minimum set of data per transaction includes: merchant ID, order ID, payment method, gross amount, fee, taxes, net amount, currency, authorization date, settlement date, and final status.

If the vendor doesn’t provide a consistent model for events (webhooks) and reports, the team ends up having to make up for it with spreadsheets. That’s why, for companies, “integration” doesn’t end with an approved payment—it ends when you can close out the month without any discrepancies.

Implementation: Technical Checklist for Businesses

If you work with an enterprise resource planning (ERP) system or business intelligence (BI) dashboards and reports, confirm from day one the format of exportable data (fields, delimiters, time zone) and how changes are versioned. A change to a column can disrupt automated processes.

Define the returns process: who initiates the refund, how the customer is notified, how it is reflected in the settlement, and how it is recorded in the accounting system (reversal of revenue vs. credit memo).

Agree with support on the incident handling process: which logs to share, response times, and how resolutions are validated. In payments, time matters because it impacts conversion rates and reputation.

If you plan to use more than one provider, establish from the outset how you will handle billing and governance: when to use each method, how to compare metrics, and how to avoid duplicate reconciliations.

Before integrating, define the data model you want to maintain: internal order, customer, method, status, net amount, fees, and dates. The finance department will use this model to close the books each month.

Decide early on how you will handle idempotence (to prevent duplicate charges during retries), how you will store tokens, and what retry strategy you will use in the event of authorization failures.

In QA, test “unfavorable” scenarios: reverse transactions, partial refunds, chargebacks, pending payments, and expired payments. The important thing is that each case leaves a consistent audit trail in reports and events.

At the operational level, set up alerts for: webhook failures, rejection rates by issuer, fraud spikes, discrepancies between settled net and expected net, and settlement delays.

Red flags to watch for when evaluating a gateway

These signs often foreshadow operational and reconciliation issues, even if the provider “charges fairly” or promises high conversion rates.

- The reports do not show the net amount per transaction, nor do they align the IDs across the dashboard, API, and exportable data.

- There are no reliable webhooks, or there is no way to reprocess events.

- The settlement statement is provided in aggregate form without sufficient detail for reconciliation.

- Refunds get "lost" in adjustments, and there is no way to track why a certain amount was deducted.

- The terms and conditions vary depending on the payment method (credit card vs. Pix vs. payment slip).

Common mistakes when implementing payment gateways

These errors occur when the focus is solely on launching the checkout process and the related operations—such as reconciliation, returns, and adjustments—are overlooked.

- Failure to define a unique and persistent order ID throughout the entire workflow (checkout, webhooks, reports).

- Reconcile using bank totals without reconstructing the net amount per transaction.

- Do not test statuses that are not "Happy" (pending, expired, partial refunds, chargebacks).

Operational example: Pix confirms quickly, but reconciliation depends on IDs. If the bank statement doesn't have a reference you can map to, you end up reconciling manually on a volume basis.

Frequently Asked Questions About Payment Gateways in Brazil

Which payment method should typically be prioritized for e-commerce in Brazil?

It depends on your audience and payment method. In Brazil, Pix is usually the preferred option due to its widespread adoption and low cost, with credit cards (and installments) as the standard and Boleto for certain segments. Track conversion rates by payment method.

How does the reconciliation statement affect accounting reconciliation?

Define which identifiers and reports you receive. Ensure that each transaction has consistent IDs and that the reports break down net amounts, commissions, and settlements.

What should I look for in the clearance sale?

Calendar, currency, fee discounts before settlement (netting), and transaction details. Also, whether there are any withholdings or adjustments that appear on the settlement statement.

What do I need to process international payments to Brazil?

In addition to the payment method, you need clarity on exchange rates (FX), crediting times, and reconciliation between the supplier, the bank, and the accounting department. See the guide to international payments.

When is it usually a good idea to use more than one supplier?

When you need redundancy, better rates per method, or a range of methods that a single provider cannot offer. The cost is greater operational and reconciliation complexity.

Sometimes a sale can be lost because, when the customer swipes the card, a declined payment notification arrives. In this article, we tell you the most common reasons why this happens and what solutions you should apply in your business to reduce its impact.

What does a declined payment mean?

A declined payment is a transaction rejected by the bank or company to which a card belongs, which means that the customer cannot complete the purchase at checkout and take the product he wanted or settle his debt by receiving a service.

Most common causes of a declined payment

There are different reasons why a card payment may be declined. Here are some of them:

- Expiredcredit card or debit card: this payment instrument has an expiration date and, once expired, you cannot use the card.

- Insufficient funds or lack of available credit: cards have a credit limit and if it is reached or exceeded there is no more credit until part or all of the debt is paid.

- Security measures of the issuing bank or card issuer: the card is blocked or rejected when there is suspicion of irregular movement or atypical payment.

- Card data errors : incomplete or incorrect card information.

- Bank or financial institution problems: sometimes there are sufficient funds, but a communication failure between the point-of-sale terminal and the bank results in a declined card.

- Error on the part of the cardholder: entering erroneous data, failure to authenticate for the payment process, or failure to use credit history responsibly.

How does a rejected payment affect your company?

A rejected payment not only represents a lost sale, but can also affect your company or business if it becomes a recurring problem when the payment method is by credit card. Among the usual problems that this can cause are the following:

Loss of immediate income

Your business stops getting the corresponding money for the payment that should have been made for a product or service.

Additional operating costs

Sometimes, fees are charged for processing payments or transactions that, in the end, do not materialize. It is also important to consider that the time invested in managing the failed collection is also wasted.

Deterioration in customer experience

The customer may choose to stop buying from your business because it is difficult for him to settle the purchase, even if he has a credit line or because he cannot choose other payment methods.

Impact on the statement of account

A declined payment may not have a major impact, but when you review all recurring cases the impact on your statement is negative because it is a significant amount.

Inconsistencies in the company's bank account balance

They can occur due to recording errors, transactions that are not accounted for or appear duplicated, as well as amounts not recognized by the bank.

Distrust in payment methods

Just as the customer experience is affected, the use of a payment method can also generate distrust in the business, even to the point of prohibiting it, even if that means losses in the future.

Solutions to reduce declined payments

In addition to having the option to pay with credit and debit cards (Visa, Mastercard, American Express), it is important that your business incorporates various payment methods so that the customer can choose the one that suits him best. For example, you can opt for payment in installments, mobile payment, digital wallets, transfers, among others.

It’s important to use payment gateways that optimize your transactions, such as Rebill, which improves the approval rate by 20% compared to the average for global payment providers processing payments in Latin America and offers automatic recovery of approximately 52% of declined payments through smart retries and automatic notifications. For example:

- Your company bills USD 100,000 per month in subscriptions. If 10% of the payments are rejected due to expired cards, insufficient funds or security measures by the card issuer, you would lose USD 10,000 each month. At the end of the year, that would be $120,000 in uncollected revenue.

- With a solution like Rebill, which recovers about 52% of declined transactions, your business could recoup more than $85,000 annually that would otherwise be written off as a loss.

A declined payment doesn't have to be a lost sale for your company! Contact Rebill and start recovering revenue with our smart reattempt solution.

Cards are an important means of payment for customers wishing to make online purchases. Currently, there are different apps that facilitate card payment. In this article, we explain what they are and the benefits they offer to your business.

How does a card payment app work?

A card payment app allows a business to receive the money from a customer's purchase by entering the card data into a reader attached to the mobile device, using a card reader, QR code or payment link. The information is then validated with the issuing bank and the funds are transferred to the business according to the established credit.

In Argentina, more and more businesses are looking for fast and secure solutions to receive payments, both physical businesses and online stores in Mercado Libre or Tiendanube.

9 apps to charge with credit cards in Argentina

In Argentina there are different card payment applications. Here we explain some of their features:

Pago Nube

In Argentina, customers can pay by debit or credit card. Pago Nube offers interest-free installment plans in the Plan Nube and the Plan Cuota Simple. Stores pay a commission according to the crediting period set for withdrawing the money: 1, 7 or 14 days.

Pago Nube takes measures such as data encryption and one-time passwords so that information is protected during transactions.

Mercado Pago

The app can be used with the card reader (Point Mini or Point Tap), with QR, payment links or accepts NFC payments by bringing your mobile device close to the customer's device. It works with debit and credit cards.

In the case of the QR code, the customer must scan it with their Mercado Pago app or other digital wallet or, if in person, bring the NFC-enabled device close to their phone. The payment will be confirmed immediately and credited to the account.

Mercado Pago uses SSL(Secure Socket Layer) protocol to protect sensitive information during payments, does not store the card's security code and allows 24-hour monitoring of payments.

Learn about other alternatives to Mercado Pago in Argentina.

PayPal

In addition to the digital wallet, it has an app that receives domestic and international credit and debit card payments. It generates a personalized Paypal.me link that you can send to your customers by message, email or social networks to make payments.

This app allows you to close sales in real time and protects your data, as it does not require you to share your bank account information. It only asks for a commission each time it receives a payment from domestic and international customers.

As security measures, PayPal does not display credit card information, works with data encryption and monitors transactions to prevent fraud.

MODE

The app is available for iOS and Android. Customers must integrate their payment button in your store to be able to pay with credit and debit cards associated with the MODO account.

The crediting term will depend on what has been agreed and you will receive the money from the sales in the bank account you have notified.

This app is backed by the Argentine banking system and protects transactions with the same security measures of the financial institution. It does not store card information, but facilitates the connection between the bank and the transaction to be made from the app.

Ualá Bis

The mobile app is available for Android and iOS. Face-to-face sales are charged by POS Mini or by QR. For remote payments, the payment link is enabled and sent via WhatsApp, social networks or mail.

Ualá Bis can be added to your Tiendanube or your own online store. Customers can pay with Visa, Mastercard, Cabal, American Express and Naranja cards. You receive immediate credit for sales in your Ualá.

In terms of security, Ualá Bis follows the PCI-DSS standard to protect user data and uses encryption algorithms to protect transaction information.

GOquotas

This platform offers customers the possibility of paying in interest-free installments with debit cards from financial institutions, prepaid or state-issued cards.

It does not have a registration fee or fixed cost, but a commission for each sale. It has the option of payment link and QR.

GOQuotas works as an intermediary. You receive the full payment of the sale in the bank account, regardless of whether the customer is late in paying the rest of the money.

Getnet

It is an application developed by Banco Santander that offers payments with credit, debit and prepaid cards in your online store. You can configure the time period for crediting the money and choose whether you receive it in your bank account or virtual wallet.

Among the security measures of this app are data protection with encryption and tokenization techniques, user identity verification and fraud detection protocols implemented by the Santander Group.

Orange Touch X

The app is downloaded to the cell phone, the reader is connected via Bluetooth and the card is charged from the phone. For each sale a percentage of commission and taxes is paid, depending on whether it is immediate credit, in 14 days or 60 days, if it is a credit or debit card.

The card reader allows charging by chip, contactless or magnetic stripe system. It accepts a variety of debit, credit and prepaid cards, such as Visa, Mastercard, American Express and Cordobesa cards.

The Naranja X app has a security center for fingerprint management, facial recognition and passwords, as well as identity confirmation with ID photos and selfie.

Ship

It is a payment platform via QR, payment link, Nave point and online store. It allows real-time payment confirmation, sales details and personalized summaries, you can choose when to credit sales, offer installments and discounts.

Nave uses advanced technology to protect financial data through encryption to prevent interception. Biometric authentication and an anti-fraud system are also available. It allows detailed tracking of each collection and validation of payments.

An option that goes beyond apps: Rebill

Rebill arrives in Argentina as the smartest digital payments infrastructure in LATAM. It is designed for companies that need to automate collections, manage subscriptions and improve the conversion of their online payments with total security.

Some advantages of Rebill' s payment gateway are:

- Multiple payment methods in ArgentinaCredit and debit cards (Visa, Mastercard, American Express, etc.), bank transfers, cash payments and digital wallets such as Mercado Pago through transfers 3.0, with the option of payment in installments.

- Hyper-customizable checkout: adapt the design, logic and even your domain to offer a checkout experience aligned with your brand, which can increase your conversion rate by up to 35%.

- Higher payment approval and recovery rates: a 20% improvement in the approval rate compared to the market average, and automatic recovery of approximately 52% of rejected payments through intelligent retries.

- Flexible recurring charges: set up weekly, monthly, annual or customized plans, with support for upgrades, downgrades, real-time cancellations and even free trial periods.

- It complies with PCI DSS level 1 certification, guaranteeing the highest standard in financial data protection in this type of platforms.

- Automated multichannel notifications: send reminders or confirmations to your customers via WhatsApp or Email without external integrations.

- Certified security: complies with PCI DSS level 1, the highest standard in financial data protection.

- Agile integration: connect Rebill to your stack in less than an hour via modern SDK or REST API with clear documentation.

- Unlike other platforms, it includes services such as subscription management at no additional cost.

Why consider more advanced solutions than a credit card payment app?

Apps are practical for small businesses, but a payment platform in Argentina like Rebill allows for checkout customization, control and management of recurring collections, and automation of payments and notifications, making it the ideal choice for businesses in Argentina looking to scale.

A certified and tokenized payment service minimizes the risk of fraud and has detailed real-time monitoring of transactions. This facilitates processes such as refunds, audits, reconciliations and provides greater confidence and transparency.

What are the advantages of using apps for card payment?

Card payment apps help businesses sell more, more securely and with fewer obstacles. In addition, it offers these advantages:

- Increased customer convenience: you can choose the payment method of your choice

- Remote collections: transactions can be managed from anywhere in the world, either in installments or cash.

- Transaction security: they use advanced encryption technologies and safeguard customer data to prevent fraud.

- Financial control: you can monitor online payments in real time and define whether you want immediate crediting or crediting on certain business days.

- Professional image: by using a recognized payment app you provide greater security and confidence to customers.

- You don't need expensive infrastructure: you only need to download the app and a commission will be deducted for the sale, there is no fixed monthly payment or minimum sales.

How to choose a card payment app?

When choosing a card payment app, these elements must be taken into account:

- Define your priorities: whether you want to receive money for in-person purchases, via payment link, QR code or card reader.

- Customer experience: it must be an intuitive and user-friendly app to facilitate purchases.

- Integrations: evaluate if they work integrated with financial entities, online payment systems or recharges.

- Customer segment: whether it is an app that works only with local payment methods or also accepts international ones.

- Business economics: take into account your sales volume, whether you offer the option of cash or installments, the commission percentage and credit terms.

Implementing a card payment app is a step towards the modernization of your business, whether you sell on social networks, in a physical store or in an online store.

But if your goal is not only to grow in Argentina, but throughout Latin America, trust Rebill, the online payment platform that will integrate the different types of payment in an automated and secure way.

Simplify your collections and offer the best payment experience to your customers with Rebill. Contact us, try our platform and start collecting by card quickly and securely.

For companies that need to collect payments in Argentina and expand to other Latin American markets without multiple integrations, Rebill is a direct alternative to dLocal.

Quick answer: The main payment methods in Colombia are PSE (bank transfer, the most widely used in e-commerce), digital wallets such as Nequi and Daviplata, credit and debit cards, and cash (Efecty, Baloto). For a company—especially one that receives payments from abroad—offering PSE and digital wallets in Colombian pesos increases conversion rates; the key operational steps are reference-based reconciliation and settlement.

Online sales in Colombia during the first quarter of 2025 reached a total value of $27.3 billion Colombian pesos, 16.4 % more than in the same period of the previous year, according to the Quarterly E-Commerce Behavior Report of the Colombian Chamber of E-Commerce (CCCE).

For total sales, 131.6 million transactions were recorded between January and March 2025, which is 15.6 % more than the first quarter of 2024. The average online consumer purchase value was $207,000 pesos (an increase of 1.3 %, compared to the last quarter of 2024.

This growth reflects not only increased consumer adoption of the digital channel, but also increased competition among e-commerce companies to attract and retain these shoppers.

In this context, offering the most widely used payment methods in Latin America is no longer optional, but a key condition for competing. If your business does not allow users to pay how they want—whether by card, transfer, cash on delivery, or digital wallets—you are losing sales. Here we tell you more.

What are the main payment methods in Colombia?

In Colombia there are different types of payment methods that can be grouped into online and offline. Below we detail each one of them:

Online payment methods

Bank transfers

Most people have bank accounts, both savings and checking accounts, and at least 15% of the population have wire transfers as one of their preferred payment methods. They also occupy 55% of the payment options in Colombia.

Payments with digital wallets or e-wallets

In the era of mobile devices, 69% of the population opts for digital payment methods such as e-wallets. The Financial Superintendence of Colombia reported that real-time transfers through digital wallets, during the second half of 2024, grew 231%, compared to the same period of the previous year.

Among the main payment options with digital wallets or e-wallets we have:

- NequiNequi: this Bancolombia application allows payments, transfers and withdrawals at no cost.

- Daviplata: Daviplata is a Davivienda platform that offers transfer services, ATM withdrawals and utility payments.

- Movii: the user can make payments, recharges and transfers through this digital wallet.

- Dale! debit card: Dale! Visa allows you to pay with Apple Pay, with no handling fee.

- Mercado Pago: can be linked to your direct account in Mercado Libre. It offers the options of bank transfers, cards, cash and recharges.

- Ualá: with the Mastercard International debit card you can make purchases in Colombia and around the world. Deposits are handled through an app.

- Lulo Bank: you can make purchases electronically or in physical stores, both in Colombia and around the world, withdrawals at ATMs of the Servibanca Green Network and payments and purchases through secure online payments (PSE).

- Tuya Pay: with the digital account you can send, pay and manage money from your cell phone or make cash recharges.

- Apple Pay: has established partnerships with several financial institutions for its use.

- Google Pay: is in an initial phase, but seeks to satisfy the need of users who are looking for greater convenience and a secure way to pay.

- Contactless: Colombia recorded that 37% of the population with a bank account preferred contactless digital payments by the end of 2024. This means of payment has increased by 85% compared to last year, thanks to the use of technologies such as NFC and QR codes.

- Cryptocurrencies: Colombia is the fifth country in the world that has adopted cryptocurrencies and approximately 10% of the population made transactions by 2024. One of them is Tether (USDT), which is commonly used in P2P platforms and cross-border payments, in networks such as Tron or Ethereum (USDT-TRC20).

Secure Online Payment or PSE

It is a centralized and standardized system that allows users to make online payments by accessing their funds from the financial institution where they have them. With Secure Online Payments a debit is made to the bank account through this system.

In the first quarter of 2025, it was the most used method with 63.1% share, given the levels of trust in this platform to directly connect bank accounts with e-commerce.

Offline payment methods

There are different offline payment methods that Colombians choose when it comes to their shopping experience. These are:

Point-of-sale (POS) terminals and card payments (debit/credit)

The Financial Superintendency of Colombia reported in December 2024 that dataphones or POS represented 7% of financial transactions in the country and were the most used channel for payments, with 42.88% of transactions.

Debit and credit cards

A study by Fiserv.com indicated that 64% of Colombians use debit cards as a means of payment and 37% opt for credit cards, including Visa, Mastercard and American Express.

Both credit and debit cards are second only to the option of secure online payments, especially for higher-value purchases where credit card financing is attractive to consumers.

It is worth noting that although credit cards are still relevant in digital payments in Colombia, their use has lost ground to more agile options such as PSE and digital wallets. These methods, which do not require card data or involve debt, are gaining preference for their simplicity, security and high adoption, especially among young users.

Cash payments

According to Fiserv.com, around 96% of Colombians make most of their transactions or payments in cash, considering that it is a safe way to avoid exposing their personal data.

In Colombia there are solutions such as Efecty and Baloto that offer the possibility of starting a purchase online and finishing it at physical points by paying in cash.

This type of payment represents between 8% and 12% of total digital transactions, and is key to including the unbanked in e-commerce, especially in regions where access to digital media is still limited.

What you should know before choosing the best payment method for your company in Colombia

Payment methods vary in terms of security, popularity and adaptation to consumer and merchant preferences. Geographic context and business characteristics also influence choice.

When determining the best payment method for your company, you should consider the following:

- Customer context: consider the customer' s age, digital habits, geographic location and the methods they value most when paying.

- It offers various payment methods: it caters to different customer profiles by combining traditional methods, such as cash and cards, and digital methods, such as mobile payment, wallets, e-wallets, payment links and buy now, pay later (BNPL).

- Transaction costs and commissions: consider how fixed and variable commissions will be applied in each method and notify users.

- Prioritize security and fraud prevention: apply methods such as multi-factor authentication or tokenization, encryption and other alternatives that comply with Payment Card Industry Data Security Standards or PCI-DSS.

- Ensures a convenient shopping experience: the customer is looking for a fast, simple and hassle-free checkout process.

- Evaluate the compatibility of the payment method with your business model: depending on whether it is a physical store or e-commerce, you can opt for credit cards, debit cards, virtual cards, digital wallets, "buy now, pay later", direct debit, real-time payments, mobile payment, among others.

- Review settlement times: take into account the time it takes to receive funds so as not to negatively affect cash flow.

- Choose a payment gateway in Colombia that is easy to integrate: choose an infrastructure that offers clear sales reports, allows you to solve payment problems and helps you grow.

What is the best choice of payment method in Colombia?

Rebill is the best provider of digital payment services for global companies that want to expand into Colombia, without the need to open a local entity. In addition, it has a presence in the main Latin American markets.

With its payment and subscription platform, you can collect the money as a local and settle the funds in USD and receive them in the country you are in.

Among its advantages it has:

- Integration in less than an hour: the connection through the robust API, SDK or its low-code integration allows you to accept multiple methods. In 5 lines of code you embed a complete checkout, with all payment methods.

- Flexible recurring payments: Accept different payment frequencies—whether weekly, monthly, or annually. Enable real-time subscription upgrades, downgrades, and cancellations. With the smart retry feature, you can recover nearly 52% of declined payments.

- Automatic compliance: each transaction goes through a validation process to detect whether it complies with local data protection, security and authentication regulations.

Ready to take your business to Colombia?Contact us and transform your payment management today!

Quick answer: In Chile, the best payment gateway supports local payment methods—credit cards (Webpay) and bank transfers—and charges in Chilean pesos. With local acquiring, you increase approval rates, settlement is fast, and you maintain clear reconciliation to settle payments abroad with full control.

Choosing the right payment gateway is not just a technical decision: it is a business decision. For companies that sell services online, having a solution that automates collections and improves conversion rates can make the difference between growth and stagnation.

In this guide we compare the best payment gateways in Chile and analyze their costs, integration and available payment methods to help you make an informed decision. Check them out below:

What is a payment gateway?

A payment gateway is a system that allows secure online payment processing. Its function is to connect the buyer with the merchant and validate the transaction between the two, either by bank card, transfer or any other digital payment method. They are widely used in e-commerce.

Top 10 payment gateways in Chile

1. Rebill

Rebill is a payment platform designed for companies with large-scale operations, both in Chile and in other Latin American markets. It is especially designed for companies that handle a high volume of transactions, in sectors such as SaaS, EdTech, HealthTech and eCommerce.

Rebill operates in Chile and allows Chilean companies to charge in Chilean pesos, and international companies to charge in CLP and settle in USD abroad, depending on the structure of the transaction. It is useful for online service businesses (SaaS, EdTech, HealthTech, eCommerce) that need configurable checkout, reconciliation, and operational tools.

Examples of companies that use Rebill in Chile: Tripleten, Henry, MSK Latam, Asegura tu viaje, Neolo, Pax Assistance.

Its solution stands out for improving conversion rates through checkout optimization and payment rules. It also boosts payment approval rates by up to 20%—above the international average—and features a retry and recovery mechanism for declined payments that recovers nearly 52% of transactions that initially fail.

Designed for regional scaling, Rebill positions itself as a scalable, reliable solution for businesses seeking efficiency and sustained growth.

In terms of security, it complies with PCI DSS level 1 certification, which guarantees the highest standard in financial data protection.

- Credit cards (Visa, Mastercard, Amex, etc.)

- Debit cards

- International cards

- Bank transfers

- Cash payments

- Installment Payments

- Rebill enables rapid implementation thanks to its robust API, flexible SDK and low-code options. In just one hour, companies can activate the system and start processing payments.

- With only 5 lines of code it is possible to integrate the checkout in your platform, enabling all payment methods.

- In addition, it offers seamless connection with systems such as CRMs, ERPs or collection tools through Make.com. It also includes webhooks, which allow you to automate real-time notifications to your internal systems.

- For foreign companies operating in Chile, commissions start at 3.50% + 50 Chilean pesos per credit card transaction, plus an additional charge for currency conversion. And for Chilean companies, the fee is 2.80% + 50 Chilean pesos + VAT.

- Unlike other providers, this platform does not charge extra for features such as subscription management.

- The exchange rates used and conversion rates are fully transparent at Rebill: they can be consulted from their website in the rates section, which also includes an online calculator to estimate the net revenue per transaction.

Flow (flow.cl)

Flow is one of the most versatile Chilean payment gateways, ideal for e-commerce companies. It accepts multiple payment methods and allows simple integrations for online stores.

- Credit cards

- Debit cards

- Prepaid cards

- Electronic wallet

- Cash payment by ServiPag

- Bank transfers via Khipu

- It has multiple integration options to suit different types of businesses. From out-of-the-box plugins for platforms such as WooCommerce, Jumpseller and Shopify, to a REST API that allows for a more customized and flexible integration for custom solutions.

- Flow Chile offers fees starting at 2.89% + VAT per credit and debit card transaction, with no monthly fixed costs, and a 3 business day crediting time. If payment is required on the next business day, then the fee is 3.19% + VAT.

Webpay Plus

Webpay Plus is the payment gateway operated by Transbank in Chile, designed to allow physical and online merchants to receive payments with different methods. It is one of the most widely used solutions in the country.

- Credit and debit cards with and without installments (Visa, Mastercard)

- Prepaid

- Redcompra

- Onepay

- Digital wallets associated with Transbank

- Webpay Plus provides APIs, SDKs and plugins that fit both custom developments and online stores already set up on platforms such as WooCommerce, Magento or PrestaShop. It also allows you to connect your physical terminals with face-to-face sales systems.

- The cost of operating with Webpay Plus depends on the type of business, the sales channel and the characteristics of each transaction.

- On the one hand, a fixed monthly charge may apply for the rental of on-site devices, such as mobile or fixed POS (except if you purchase Mobile POS equipment).

- On the other hand, each sale generates a commission composed of a variable fee -which includes the interchange fee and the branding costs of the cards- and a fixed fee that remunerates Transbank's service (from 0.001784 UF per transaction).

4. Mercado Pago

MercadoPago, part of MercadoLibre, is a robust option for those who sell on social networks, marketplaces or their own sites.

- Credit cards

- Debit cards

- Bank transfers

- Interest-bearing installments

- Balance in MercadoPago account

- Mercado Pago offers different forms of integration, from payment links and buttons that do not require programming, to more advanced options such as Checkout API to customize the entire process. It also has plugins for ecommerce, SDKs and pre-designed modules that easily adapt to your website.

- The fee for instant crediting is 3.19% + VAT per transaction, valid for all payment methods.

5. Easy Payment

Pago Fácil is a Chilean platform designed for SMEs and companies looking for a simple option to accept payments.

- Webpay Plus

- Credit and debit cards

- Prepaid cards

- Bank transfers

- Cash

- Pago Fácil allows you to integrate your payment gateway through Plug & Play options with platforms such as Shopify, Bsale, Jumpseller and WooCommerce. You can also connect through its API. In addition, it offers features such as payment buttons and links, ideal for selling through social networks or without the need for a website.

- For micro and small companies, Pago Fácil charges a commission of 2.95% + VAT per transaction, with no fixed costs or transaction limit. This plan applies to legal entities with annual sales of up to 25,000 UF. For medium and large companies, the fees are personalized and are defined together with a commercial executive.

6. Payku

Payku is a Chilean fintech that offers a simple platform to implement digital collections.

These are the payment methods offered by Payku:

- Debit cards (Redcompra, Visa and MasterCard)

- Credit cards (Mastercard, Visa, American Express, Magna and Diners)

- Bank transfers

- Cash

- Payku offers ready-to-install plugins for popular shopping carts such as WooCommerce, PrestaShop and OpenCart, allowing you to activate the payment gateway in a matter of minutes.

- Payku's commissions for card transactions is 2.99% + VAT, with the money credited the next business day. For the rest of the payment methods vary between 1.99% + VAT and 2.99% + VAT.

7. PayU

Although its presence is strongest in Peru, Ecuador and other LATAM countries, PayU also operates in Chile. It is ideal for companies that require a multi-currency system.

Learn about the payment methods that PayU has available in Chile:

- Credit/debit cards

- Bank transfers

- Cash payments

- For integration, PayU offers everything from out-of-the-box options such as WebCheckout, to more advanced solutions via API or SDK, ideal for those looking for a customized payment experience within their website.

- PayU fees vary by country, payment method and transaction volume. On average, the cost per processed sale is around 3.49% per transaction.

8. PayPal

PayPal is still one of the best known options globally, although its presence in Chile is smaller. It can be useful for international payments or customers who already have an account on the platform.

The payment methods offered by PayPal are:

- Credit cards

- PayPal Balance

- Linked bank account

- PayPal Checkout works with payment buttons and APIs to easily integrate with your eCommerce, allowing you to receive payments quickly, securely and seamlessly for your customers.

- In Chile, PayPal fees for receiving payments vary according to the total amount of sales in the previous month. For example, if your business receives between USD 0.01 and 3,000.00, a fee of 5.40% + a fixed commission applies. The higher the amount of sales, the lower the fee to be paid.

9. Kushki

Kushki offers online payment solutions for businesses in Latin America, including Chile. It was founded in 2016 with the goal of connecting the region through digital payments.

The payment methods available with Kushki are:

- Credit and debit cards (Visa and MasterCard)

- Transfer

- Cash payments

- It offers flexible integrations through APIs and plugins for e-commerce platforms, facilitating the implementation of its services in various digital environments.

- Kushki's rates are not disclosed on their website; however, they inform that in addition to a transaction fee, they apply monthly billing minimums, which are defined according to the volume of your business. For specific details, it is necessary to contact their sales team.

10. Khipu

Khipu is a Chilean payment gateway that allows direct bank transfers as an online payment method, without the need to enter data manually.

- Simplified bank transfers from various Chilean banks.

- Payments through digital wallets and prepaid accounts.

- On-site payments with QR code.

- Khipu has plugins for platforms such as WooCommerce, Shopify and Prestashop, as well as APIs that allow custom integrations with websites, mobile apps or internal systems. It also has tools such as payment links and payment buttons that can be shared via WhatsApp, email or social networks, making it easy to adopt without the need for advanced technical knowledge.

- Khipu charges a commission of 0.69% + VAT on the amount collected for instant payments through bank transfers, with additional discounts for volume of transactions.

- For businesses that prefer a fixed rate, there is the option of paying UF 0.0105 + VAT per transaction.

- In the case of automatic payments or subscriptions, fees vary from UF 0.0056 + VAT per transaction, depending on the type of agreement selected.

What to consider when choosing a payment gateway in Chile?

When integrating a payment processing platform, it's important to look beyond price. Here are some key variables you should consider depending on the size and needs of your business:

Available payment methods

Look for a payment platform that allows you to receive payments with various payment methods. The more payment options you offer, the smoother the purchase process will be for your customers and therefore, the more your business will grow.

Ease of integration

Choose a payment gateway that makes implementation easy, either through out-of-the-box plugins, low-code integrations or a well-documented API. Some platforms, such as Rebill, also offer native connectors with systems such as ERP, CRM or ecommerce, which simplifies data synchronization.

Local and regional support

If your company operates in several Latin American countries or has expansion plans, it is advisable to choose a platform with regional presence and support in Spanish to resolve questions quickly.

Extra functionalities

Explore whether they offer tools such as subscriptions, recurring payments, automatic reconciliation, webhook notifications, rejected payment recovery logic or checkout customization. These features can improve efficiency and increase conversions.

Improved conversion rate and payment approvals

A good payment gateway doesn't just collect payments: it also optimizes them. Choosing a solution that offers agile payment flows that adapt to user behavior can increase your conversion rate. You can improve conversion with checkout optimization and payment rules. While the approval rate could increase by up to 20%, this translates into more sales.

Scalability

If your business is growing, make sure that the gateway you choose can accompany you to new markets or support a higher volume of transactions without problems.

---

Conclusion

In a competitive market like the Chilean one, having a gateway that optimizes your collection is key.

After learning about these 10 alternatives, Rebill is positioned as a solution designed for companies with high volume operations seeking to grow in Chile and Latin America, without technical friction or loss in the payment experience.

If your operation requires a tool that evolves with your business, we are your best ally.

Contact us and find out how we can help you scale your business sales.

----------------------

Disclaimer

This content is for informational purposes only and was prepared based on publicly available information from the official websites of each payment gateway in Chile at the time of writing (July 2026). Rates, terms, and features are subject to change without notice; therefore, we recommend contacting each provider directly for the most up-to-date information.