Share this article

No items found.

No items found.

The definitive guide to expanding your business in LATAM.

A FREE 5-day email course that teaches you how to optimize your payment rates and simplify your operations.

Obtain the guide

In Latin America, payment processors have become an indispensable mechanism for business growth (physical and digital), thanks to digitization and the growing adoption of electronic payment methods.

These systems allow agile transactions adapted to the particularities of the regional market. Stay to find out which is the best payment processor option to automate your business collections.

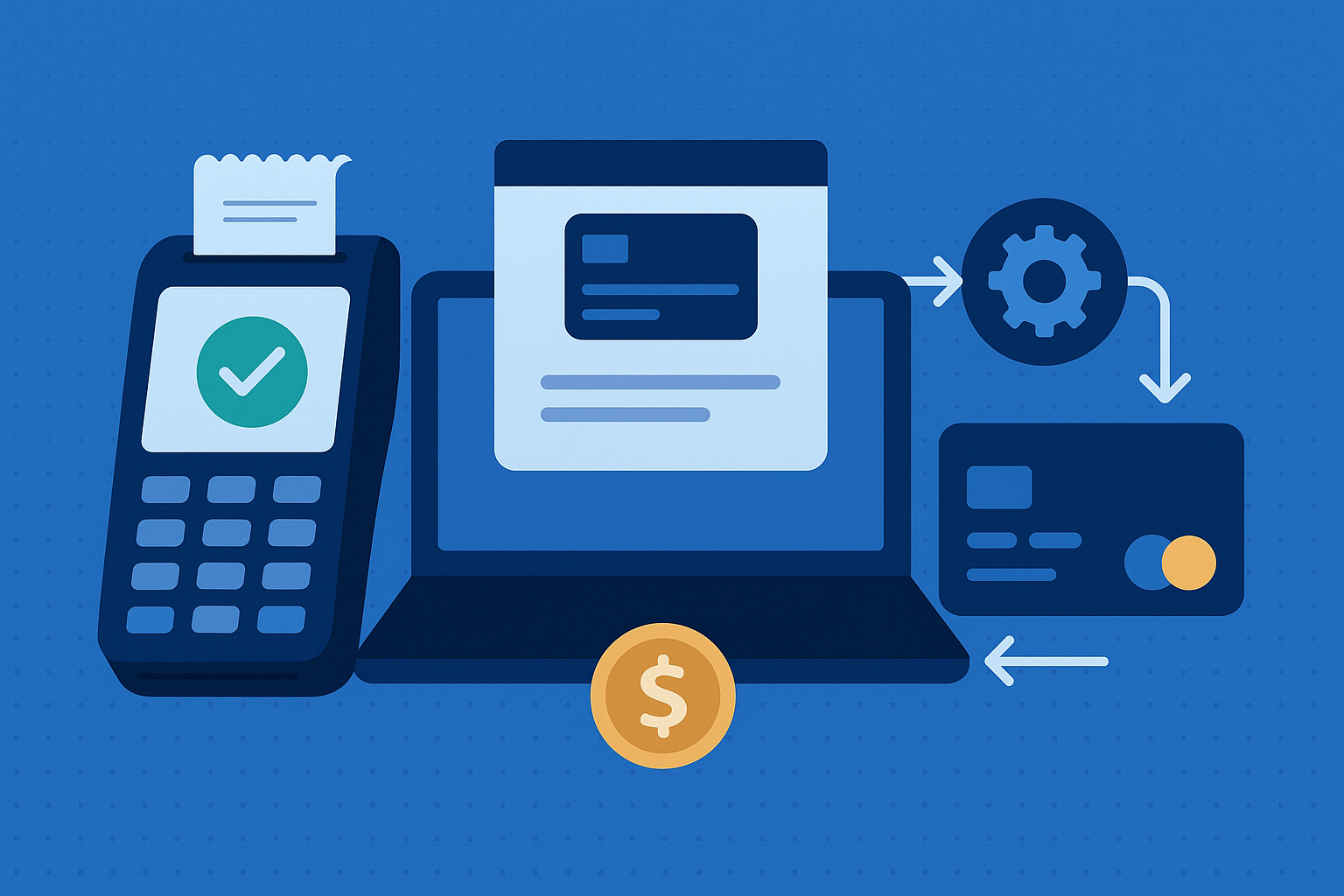

A payment processor is a system that manages electronic transactions between a buyer and a seller during a commercial operation. It is essential both in e-commerce and in physical stores, since it allows receiving payments with credit cards, debit cards, digital wallets and other electronic payment methods.

By functioning as the intermediary between the client's account and the merchant's account, it ensures the mobilization of funds in a secure and efficient manner.

When making electronic payments it is important to understand how they work and what is the difference between a payment processor and a payment gateway. Although they work together, each one fulfills a specific role.

Apayment gateway is responsible for collecting the customer's payment information and securely redirecting it to the payment processor or acquirer to complete the payment. Some popular payment gateways in Latam are: Rebill, Mercado Pago, Kushi, among others.

On the other hand, thepayment processor is responsible for processing transactions, connecting the acquiring bank, the issuing bank and the card network (such as Visa, Mastercard or American Express), i.e., the processor is the link that ensures the movement of money between financial institutions.

Thus, the key difference between gateways and processors is that: the gateway captures, encrypts and transmits the payment data, while the processor handles the authorization, communication and transfer of funds.

Paying through a service with payment processors is a quick and easy payment experience. However, this mechanism is complex and requires the fulfillment of a series of steps:

The process begins when the customer decides to make a purchase, either in a physical store (through a point-of-sale terminal) or online (through a payment gateway such as Rebill, Stripe, Checkout or PayPal).

The customer enters their payment information, such as cardholder name, card number, security code, digital wallet, etc.

The payment gateway then collects and verifies the data entered by the customer, making sure that the information is valid and that the card is not expired or blocked. The payment processor also verifies that the data matches the issuing bank's records.

To protect transaction data, the information is encrypted and, in many cases, tokenized (i.e. replaced by a secure identifier). This step is essential to prevent fraud and ensure the security of sensitive data. Learn more about tokenization.

The encrypted information is sent to the acquiring bank, which forwards it to the card network and then to the customer's bank, which validates the transaction, reviews the available funds and authorizes or rejects the payment. The response then travels back the same way to the point of sale.

If the transaction is approved, the payment processor records the authorization and the merchant can deliver the product or service to the customer. The funds are reserved in the customer's account pending final settlement.

Finally, the issuing bank transfers the funds to the acquiring bank. The acquiring bank then deposits the money into the merchant's account, completing the process. Depending on the payment system, settlement may be effective in real time or take a few business days.

All of this happens in a matter of seconds, ensuring a fast and reliable experience for both the customer and the merchant. This is how the processor proves to be of paramount importance for payment services in the digital and physical world.

Choosing the right payment processor for your business is a decision that needs to be made carefully, as it will impact your customers' experience. Among the factors to consider when choosing the best payment processor are:

Processors as a method of optimizing online payment methods have become key players in e-commerce in Latin America. Here are some of the most popular payment processors in the region:

Rebill is a payment infrastructure, ideal for companies that manage subscriptions or digital services. It is present in the main Latin American markets:

It is one of the most recognized payment processors in Latin America, with a wide scope and versatility. Noted for:

Kushki is an emerging fintech that facilitates the implementation of electronic payments for digital businesses. It is characterized by:

It is present in more than 200 countries and is widely used in Latin America. It stands out for:

PayU has a strong presence in emerging markets and is trusted by regional businesses. It has:

Rebill is positioned as the ideal option to give dynamism to your digital payments. Its infrastructure is designed so that your business can grow smoothly, offering a seamless experience for both you and your customers. Contact us and discover an efficient payment service provider for your business.

.avif)