Share this article

No items found.

No items found.

The definitive guide to expanding your business in LATAM.

A FREE 5-day email course that teaches you how to optimize your payment rates and simplify your operations.

Obtain the guide

Discover in this article how interest-free months work, their benefits and why they are key to the success of your business.

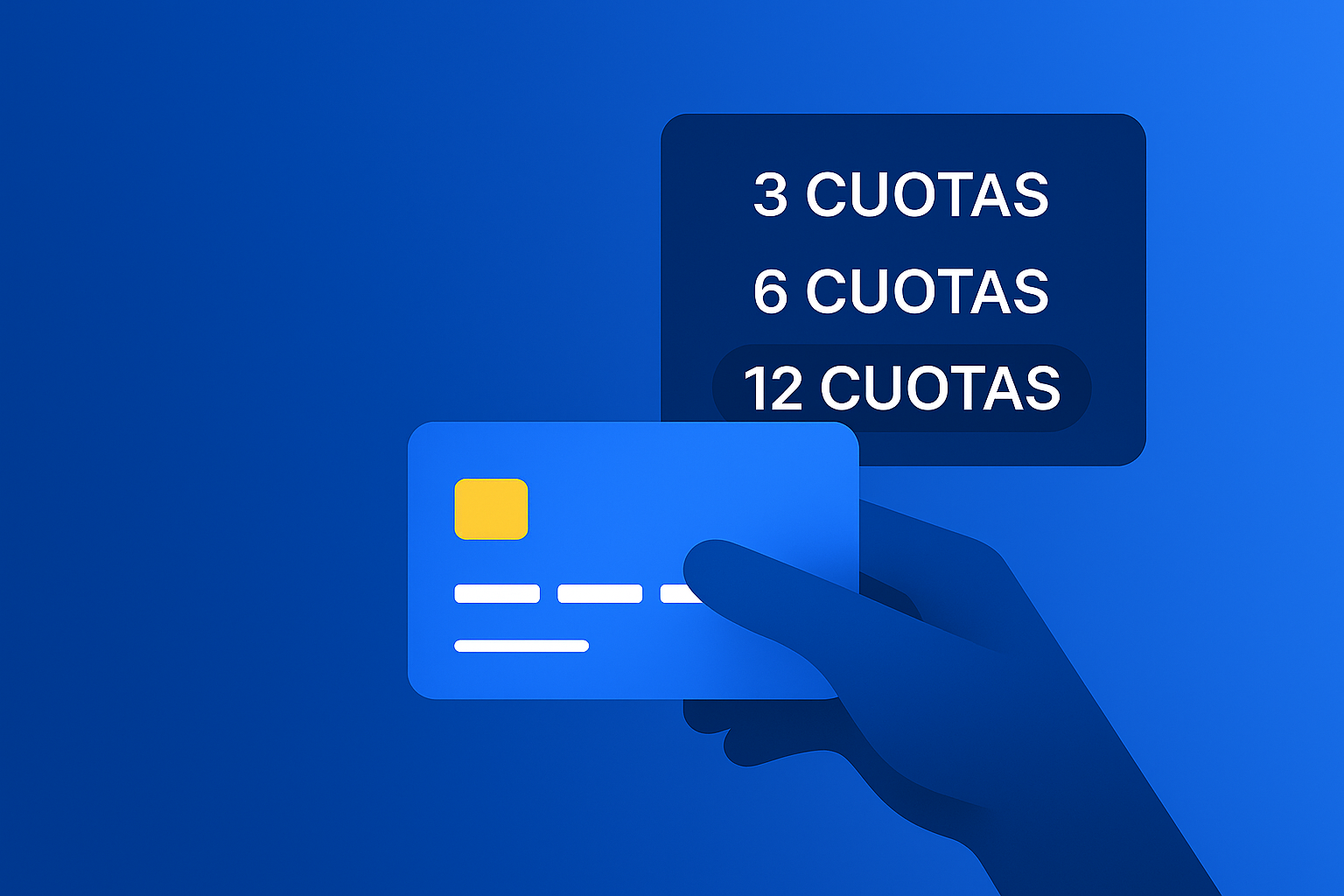

Months without interest (MSI) is a promotional method offered by credit cards that allows individuals to obtain products or services by paying in fixed monthly installments, without generating additional interest.

This financial tool has become very popular in Latin America, especially in Mexico, by encouraging consumption, increasing conversion and reducing purchase friction, which is very attractive especially for e-commerce, retail and sectors such as Edtech.

When you make a purchase with interest-free months, the total amount of the product or service is divided into established monthly installments (such as 3, 6, 12 or more months). Each installment is paid in the agreed term until the total amount of your purchase is paid in full.

For example, if a customer purchases a personal finance course for $1,200 MXN in 12 months interest-free, he will pay $100 MXN each month, with no extra charges.

To make a purchase at months without interest, follow this process:

The consumer only makes a minimum monthly payment, but the total amount of the purchase will be taken into account from the credit line of the card. In other words, it affects the credit limit.

Interest-free months make products and services more accessible in different sectors and at different times of purchase:

Likewise, interest-free months can be applied in various contexts, allowing consumers to take advantage of them at specific times, such as:

Selling on interest-free months provides companies with strategic advantages that impact their sales and competitiveness. This can be a decisive factor. The main benefits are detailed below:

By facilitating the purchase of products and services interest-free, one of the main barriers to purchase, which is the ability to pay immediately, is eliminated. This motivates more customers to make their purchases, which generates an increase in sales volume.

Customers often take advantage of interest-free months to access higher-value products or goods, since payment is divided into installments. This increases the average value per transaction and encourages the consumption of high-value goods and services.

Interest-free monthly payments allow companies to stand out in the market and attract new customers who value payment facilities.

By providing flexible payment solutions, merchants improve the shopping experience and strengthen the relationship with their customers. This drives loyalty and repurchase, which are key to sustained growth.

In most cases, through agreements with the bank or payment gateway, the merchant receives the full amount of the sale from the beginning, while the customer pays the minimum amount in monthly installments. This means greater liquidity and reduced collection risk for the company.

These advantages provide the ideal context for businesses to take advantage of solutions such as Rebill, a payment platform that promotes the integration and management of MSI across multiple channels, further enhancing the growth and professionalism of your business.

Although in Mexico there is no specific regulation governing interest-free months, there are some conditions that companies should consider, among which are:

To offer interest-free months, merchants must enable this function through a specialized payment platform or through direct agreements with credit card issuing banks.

The platform is in charge of processing the transaction, deducting the corresponding commissions and coordinating with the bank the monthly payments that are reflected in the customer's card.

The process is simple and safe:

It should be noted that not all platforms offer MSI automatically, some require manual activation or meet specific conditions.

Rebill makes it easy for companies to provide interest-free payment options automatically, managing total merchant collection, bank coordination and transaction security, all conveniently integrated into your system.

Sell more by giving your customers what they want: interest-free monthly payments. Find out how to activate them safely without losing profitability with Rebill,talk to us and we'll tell you how!

.avif)